As the year draws to a close, many around the world find themselves in various seasons of celebration, relaxation, and for some, the tradition of gift-giving. Years ago, Black Friday reports would be accompanied by stories of frenzied mobs bursting through store doors as bargain hunters sought to secure their loot. There are even TikTok videos poking fun at the situation, with comments suggesting that the masses were the result of better deals in the past. Some have remarked that inflation could be the cause for less exuberance, which sadly, is the case for some. This holiday season, a basket of goods costs 18% more than it did before the pandemic. However, I think the more obvious solutions for why we don’t see frenzied activity at the brick-and-mortar stores anymore are the same reasons why so many retailers are shrinking their real estate footprint altogether – digitization and ecommerce.

It’s not that stores were ignored, but the preference for online is evident. Square remarked that “in-person shopping increased 15%, while online cart sizes were 3.9X higher than [physical]”. Buy Now, Pay Later (BNPL) transactions through Afterpay jumped 19%, a similar gain was recorded at rivals Klarna and Affirm. Overall, U.S. digital purchases on Black Friday this year hit an all-time high of $9.8B, up 7.5% compared to 2022 and Cyber Monday came in at $12.4B, or 9.6% higher year-over-year. Shopify announced that their SME merchants around the world generated $9.3B in sales this Thanksgiving. Notably, their one-tap checkout option with BNPL functionality, Shop Pay, saw 60% increased adoption. These examples serve to underscore how technology platforms are benefitting from the continued digitization of commerce and innovative product suites.

The figures above might have you believe that the related equities are performing well, and depending on your timeframe, you’d be correct. In the past month, Square, Shopify and Affirm are up 64%, 58%, and 99%, respectively. However, they’re all down significantly from the heights of the post-pandemic boom.

Normalized Equity Performance

You could plot similar charts of most fintech/embedded finance stocks and the related ETFs. Since the euphoria of the illusory growth during Covid, the valuations of the platforms above have declined meaningfully, but their sales have grown consistently. Of course, sustainable profits remain to be seen.

Select Financial Metrics

The thing about valuations is that, while they’re meant to be underpinned by fundamentals like discounted cash flows, the crowd’s prevailing opinion often matters more in practice. Simon Taylor of FinTech Brainfood recently noted, “Narratives are powerful, but the crowd chases consensus… Rates didn’t kill growth… The crowd got crushed.” Leading him to conclude, “Rumors of FinTech’s demise were overstated.”

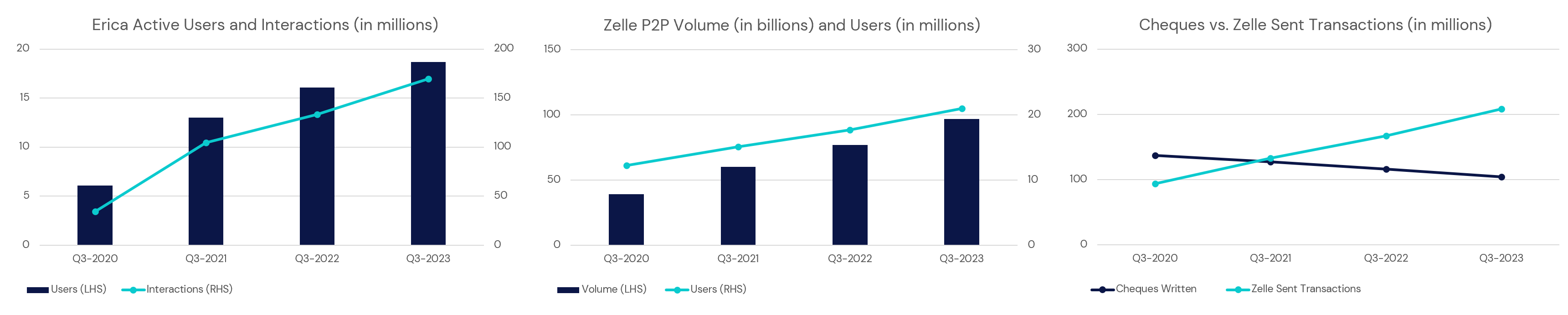

I agree with Simon’s assessment. Multiples and sentiment will ebb and flow, but there’s a clear trend towards digitization, mobile banking services, and embedded finance. We are only three quarters into the year, yet there have already been over 800,000 mentions of “digital” and related terms in the financial industry's corporate disclosures, as collected by Bloomberg. This marks the third consecutive year of such a significant focus on technological transformation in the sector. Bank of America’s Q3-2023 earnings presentation provided evidence of these themes as well. Their AI financial agent, Erica, and (technically Early Warning Services’) peer-to-peer payments network, Zelle, continue to be favoured over legacy transaction channels.

Bank of America Consumer Digital Volumes

As McKinsey notes, following a period of excitement, FinTechs are now entering “a new era of value creation, where the focus is on sustainable, profitable growth”. The path forward will be characterized by more thoughtful expansion and cost discipline. Bloomberg reported that 4,200 FinTech staff (about 11% of all startup employees) were let go in H1-2023, with more likely to come. Sell side research covering the space in Q3 highlights that these topics are front of mind. What’s encouraging is that the stocks of many such companies have exploded higher since the quarterly earnings. The market is supportive once again.

Looking at the underlying holdings of the FinTech ETFs listed in the U.S., you’ll notice some digital asset exchanges and miners. It’s natural to categorize crypto service providers as operators of financial technology. 24/7 trading and easily accessible leverage have likely amplified the industry’s cyclicality, but the same themes apply. Ours is a story of broad-based digitization. The crowd got ahead of itself in 2021, and higher interest rates caused a reshuffling of capital, which cleared out many margined traders and even some bad actors. Both BNPL and crypto have caught the watchful eye of regulators, as well. Despite challenges, these ecosystems continue to thrive, adapting to leaner times with improved resource management. Innovations are steadily introduced, signaling readiness for the next growth cycle.

The increased usage of BNPL during Cyber Week is worthy of our attention. It may be that shoppers simply prefer the cash flow enhancement, but it could also indicate that the buyer is getting stretched. Especially as the feature is being used to purchase gas and groceries. Given the consumer’s importance in GDP growth, one logical extension is that the economy is slowing, and this carries monetary policy consequences. A more relaxed stance from central banks should be supportive of assets like Bitcoin but a recession could pose risks for BNPL lenders. It will be interesting to see how the coming quarters playout within the Fintech verticals, too.

Aquanow specializes in unlocking digital asset potential for financial institutions. Contact us to explore how our expertise can enhance your performance.

If you want to contribute to the web3 movement, Aquanow is on the look for curious and motivated folks to join our team. Feel free to reach out directly or check out the current openings here.

.png)