The asset management industry is emerging as a key battleground for blockchain adoption in the “Web2.5” era. As expected, rather than a wholesale shift, we’re seeing methodical steps by traditional financial institutions to explore tokenized products, blockchain-based settlement, and digital-native infrastructure for investment operations. These moves represent a broader transformation in how financial assets are issued, traded, and held.

At the center of this shift are initiatives like:

- the SWIFT-UBS-Chainlink pilot, which explored blockchain as a back-end infrastructure for subscription, trading, and settlement,

- the development of tokenized investment funds, and

- the emergence of institutionally issued stablecoins.

Together, these innovations reveal how asset managers are adapting blockchain to fit into familiar frameworks while laying the groundwork for a more digitally native future.

Connecting Legacy Systems to Blockchain Settlement

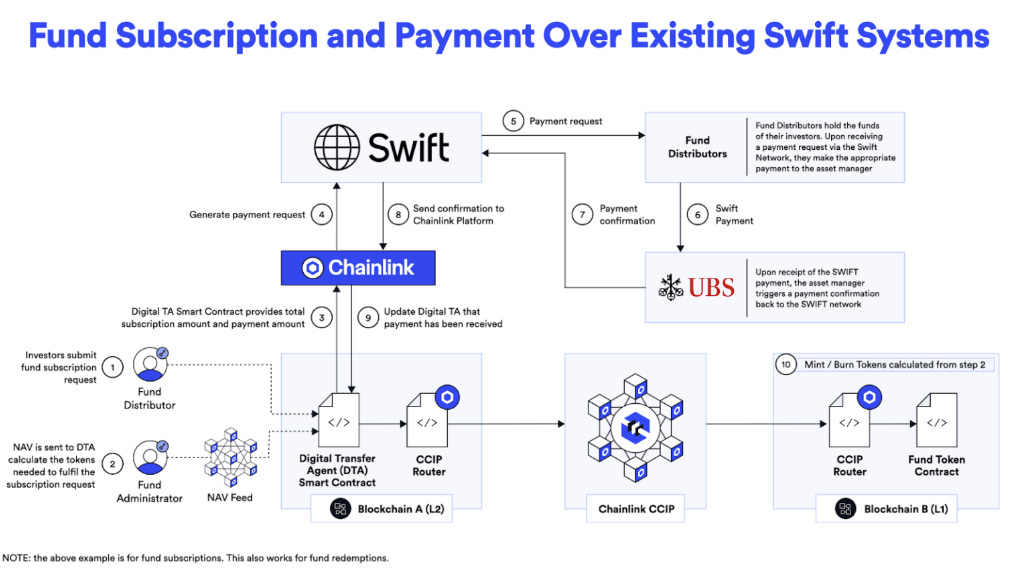

SWIFT, the backbone of global financial messaging, is working with Chainlink to explore blockchain’s potential in payments and settlement. While this partnership is broad in scope, one of the most compelling test programs focused on the lifecycle of assets and data as it relates to the fund management.

As highlighted in a recent discussion between Chainlink's Sergey Nazarov and SWIFT's Giles Goh and Andrew Wong from UBS, the pilot—part of the Monetary Authority of Singapore’s (MAS) Project Guardian—demonstrated how blockchain can support secure, real-time settlement of tokenized assets across multiple private and public blockchains. It enabled asset managers like UBS, custodians like SBI, and clearinghouses to use SWIFT’s existing messaging rails while leveraging Chainlink’s Cross-Chain Interoperability Protocol (CCIP) and a new digital transfer agent (DTA) smart contract to coordinate actions.

A major breakthrough in the SWIFT-Chainlink endeavour involved automating fund subscriptions and redemptions. Off-chain fiat payments were linked to on-chain fund tokens that could be automatically minted or burned—enabling seamless lifecycle automation for tokenized investment products. Crucially, this integration worked within existing financial infrastructure, requiring no overhaul of global systems.

The implications are substantial. If adopted at scale, blockchain-based settlement could:

- Reduce counterparty and settlement risk

- Enable near-instantaneous clearing for assets like government securities and funds

- Increase liquidity in global markets

- Automate complex workflow processes

These are not just theoretical benefits. SWIFT is already running live trials for digital asset payments and has a line of sight to a production-ready solution by late 2025 or early 2026. This is a pivotal moment for the integration of digital assets into traditional financial architecture—but one that will unfold gradually due to the continued importance of compliance and risk management.

Tokenized Funds: Programmability Meets Familiar Structure

Tokenized funds are gaining traction as a way to merge blockchain benefits with the familiar operating model of traditional asset management. Firms like Franklin Templeton and UBS are launching or testing funds issued and maintained on public blockchains. These funds offer:

- Fractional ownership and increased liquidity

- Transparent fund operations

- Programmable compliance and access controls

The recent pilots from UBS, SBI, Chainlink, and SWIFT highlight just how transformative tokenized funds can be. These initiatives tackle long-standing inefficiencies in traditional fund administration—where fund creators, custodians, distributors, and administrators operate across fragmented systems—with a blockchain-based architecture that offers unified, real-time coordination.

At the center of this new approach is the concept of a Unified Golden Record—a smart contract that tracks the full lifecycle of a fund (NAV calculations, subscriptions, redemptions, etc.) across multiple blockchains. Oracle networks, such as Chainlink, bring off-chain data (e.g., Net Asset Value) on-chain, enabling automated execution and verifiable recordkeeping. UBS played the role of fund manager, SBI as custodian and distributor. Watch this to learn more.

The benefits of this on-chain architecture are wide-ranging:

- Tokenized fund shares can be issued across multiple chains (private and public), improving cross-chain liquidity, accessibility, and control.

- Chainlink’s CCIP ensures interoperability between these chains, while preserving compliance.

- Swift’s integration allows off-chain payments (e.g., wire transfers) to interact with fund contracts—eliminating the need for investors to hold crypto wallets.

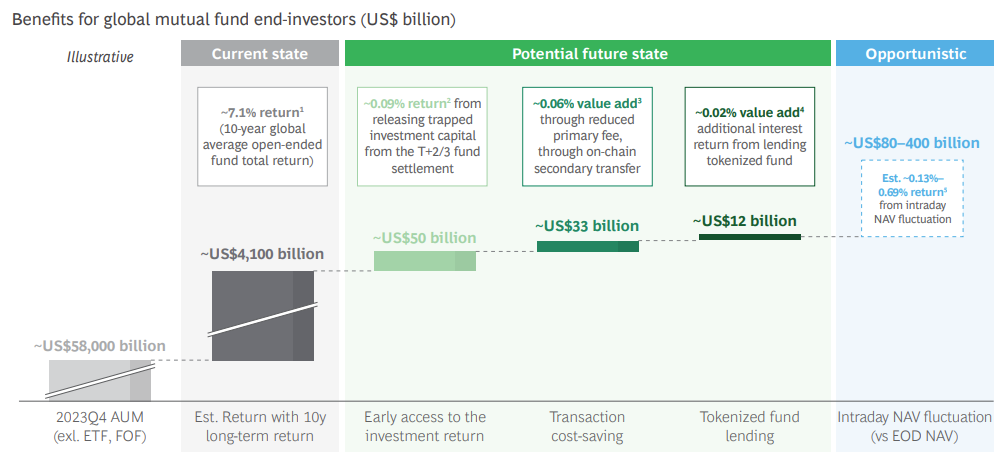

Importantly, this design aligns with the regulatory landscape. The pilots emphasized jurisdictions with mature digital asset frameworks and embraced a B2B2C model to ensure compliance and control. Putting fund performance and operational data on-chain also opens up new dimensions of product design—enabling faster redemptions, easier audits/tax reporting, and greater transparency for investors and regulators alike.

While other fund strategies—such as equity, credit, and venture—have been experimented with in tokenized form, money market funds have been the most successful. Their deep liquidity, cash-like collateral, and yield profile make them an ideal starting point. Perhaps more importantly, they provide a direct link to a fundamental element of blockchain finance: stablecoins, which often derive their backing from the same high-quality liquid assets that comprise these funds.

These tokenized funds aren’t just novel wrappers—they represent a step toward making all financial instruments more composable, accessible, and programmable. As regulatory frameworks mature, tokenized funds could become the default for managing both traditional and digital assets.

Stablecoins: Digital Cash for On-Chain Asset Management

Adding further momentum to this transformation and creating a new front on the battleground for blockchain adoption is the emergence of institutionally issued stablecoins. Fidelity Investments is reportedly engaged in advanced testing of its own stablecoin, designed to act as digital cash within its Treasury Digital Fund money market offering. The product, filed recently for launch on Ethereum, is a tokenized vehicle providing exposure to U.S. dollars and Treasuries “to be used primarily by participants in the broader blockchain ecosystem”.

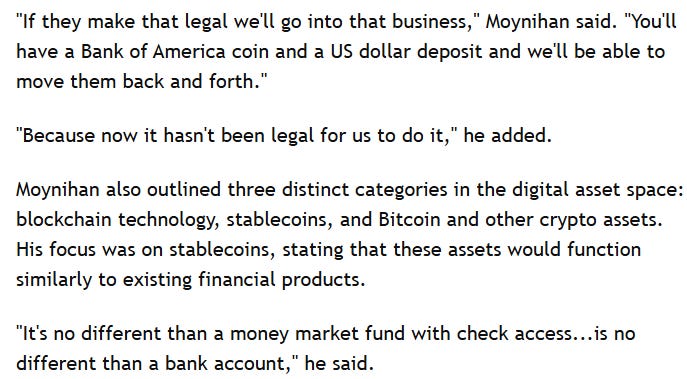

According to a Financial Times report, Fidelity’s stablecoin will be used for on-chain settlement and fund flows within the Treasury Digital Fund, reflecting a broader trend: stablecoins are gaining broader acceptance as a superior way to hold and transfer value. Comments from Bank of America’s CEO, Brian Moynihan, indicate a future with very broad adoption:

Other major players aren’t far off. Franklin Templeton recently enabled investors to the convert USDC stablecoin to U.S. dollars to fund their investment in shares of the Franklin OnChain U.S. Government Money Fund. Meanwhile Blackrock’s USD Institutional Digital Liquidity Fund (BUIDL) makes up 90% of collateral backing Ethena Lab’s digital dollar, USDtb.

Both traditional financial giants offer tokenized money market funds with over $2 billion in combined assets under management and now have direct ties to stablecoins. Interestingly, Ethena is backed by Franklin Templeton, too. So far, the stablecoins issued by incumbent asset managers are not designed to compete with retail payment tokens like USDC, USDT, or PYUSD. Instead, they are institutional tools—purpose-built to enable frictionless, on-chain capital flows in a tightly controlled compliance environment. As adoption grows, they may underpin much of the operational plumbing for blockchain-based asset management.

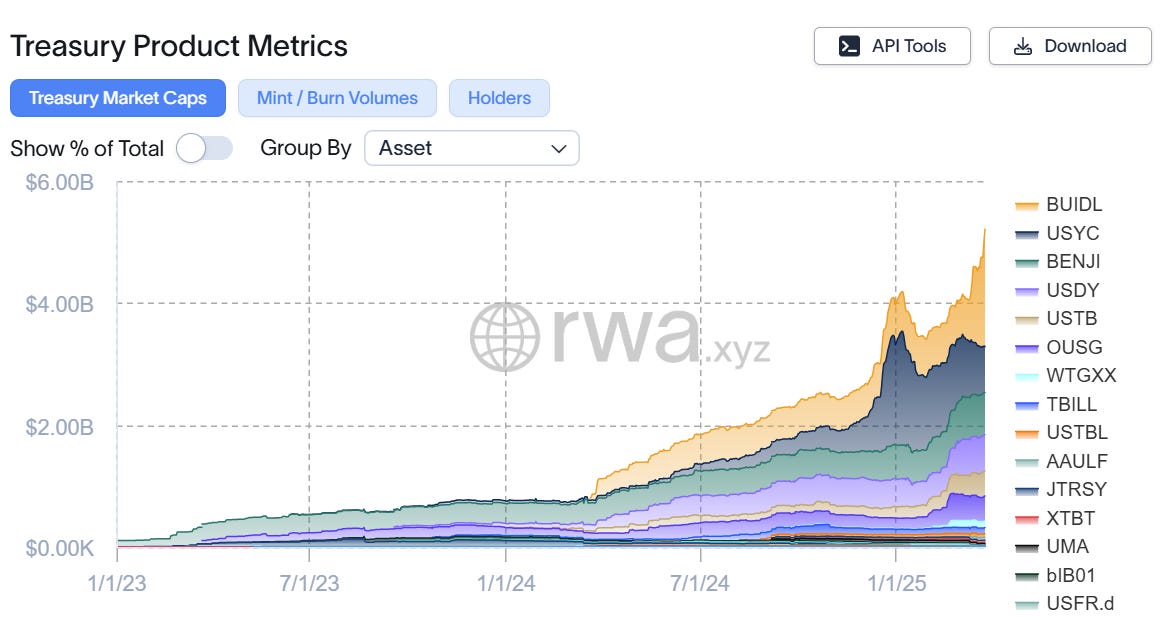

As of early 2025, the tokenized government bond fund sector has surpassed $5 billion, per RWA.xyz, which is tiny compared to the broader stablecoin market ($220B+), and a rounding error in the context of currency markets overall (Global M2 Money Supply ~$130T+). Blockchain’s gaining ground, but it’s early days.

A Measured but Meaningful Evolution

Despite headlines suggesting rapid transformation, the truth is that institutional adoption will remain gradual. Asset managers are bound by regulatory obligations, fiduciary responsibility, and deeply ingrained cultures of risk management. These guardrails slow down deployment—but they also ensure that integrations are thoughtful and lasting.

Still, the momentum is real. Strategic pilots like SWIFT-Chainlink are producing measurable results. Tokenized funds are proving their utility in production. And now, institutionally issued stablecoins are emerging as core infrastructure.

This thoughtful evolution is the hallmark of Web2.5: not a radical break from traditional finance, but a phased modernization driven by credibility, utility, and institutional standards. As blockchain infrastructure matures and regulatory frameworks solidify, asset managers will increasingly serve as the crucial bridge between traditional finance and digital innovation, carefully integrating the best of both worlds to deliver enhanced value to their clients and the broader financial ecosystem.

Aquanow’s Role in the Transformation

As traditional finance and blockchain technology continue their measured but meaningful convergence, Aquanow stands at the forefront of this transformation, building essential bridges between institutions and digital asset markets. Through strategic partnerships with established banking groups in key global markets and compliance-focused collaborations with regulated custodians, Aquanow exemplifies the Web2.5 approach—providing the specialized infrastructure, liquidity, and expertise that allows traditional players to confidently enter the digital asset space without compromising their risk management standards.

While headlines may suggest a rapid revolution, the reality is a deliberate evolution where incumbents increasingly partner with digital asset specialists rather than building capabilities in-house. Aquanow continues to strengthen these connections globally, ready to support financial institutions as they navigate this changing landscape—carefully, deliberately, and with enterprise-level requirements firmly in mind.

.png)