TL/DR: Unsecured crypto lending: more liquidity, less lockup, powered by real-time verification tech and analytics. Risks remain, but the future’s taking shape.

The 2022 crypto crash wasn’t just a market dip—it was a wake-up call against lending gone wild. Poor risk management, a lack of proper disclosures, unverifiable financials, and reckless collateral recycling cascaded into widespread liquidations, plunging asset prices and eroding trust. While overcollateralized DeFi loans held up, their rigid capital requirements underscored critical inefficiencies in digital asset lending markets.

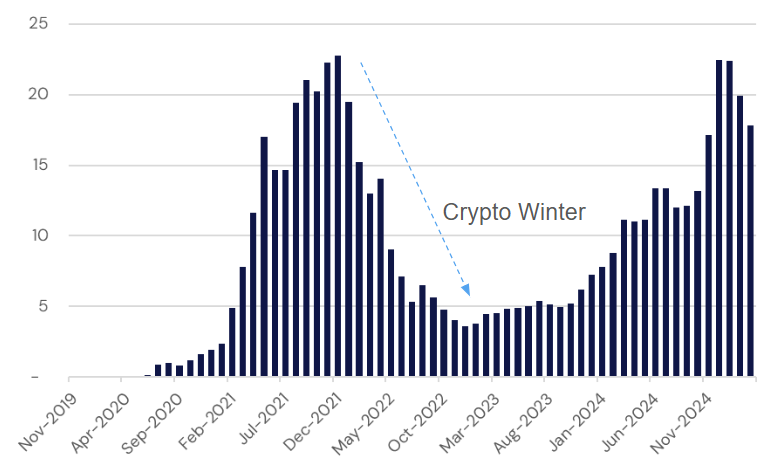

Loans Outstanding Across Top 20 DeFi Lending Protocols (in billions, USD)

Fast forward to 2025, and an emerging innovation—unsecured crypto lending—is beginning to unlock capital efficiency while expanding financial inclusion. By shifting from collateral-based models to credit-driven markets, unsecured lending could enable broader participation and more dynamic liquidity flows. In collaboration with Accountable and Agio Ratings, we explore the evolution, opportunities, and risks of this transformative trend.

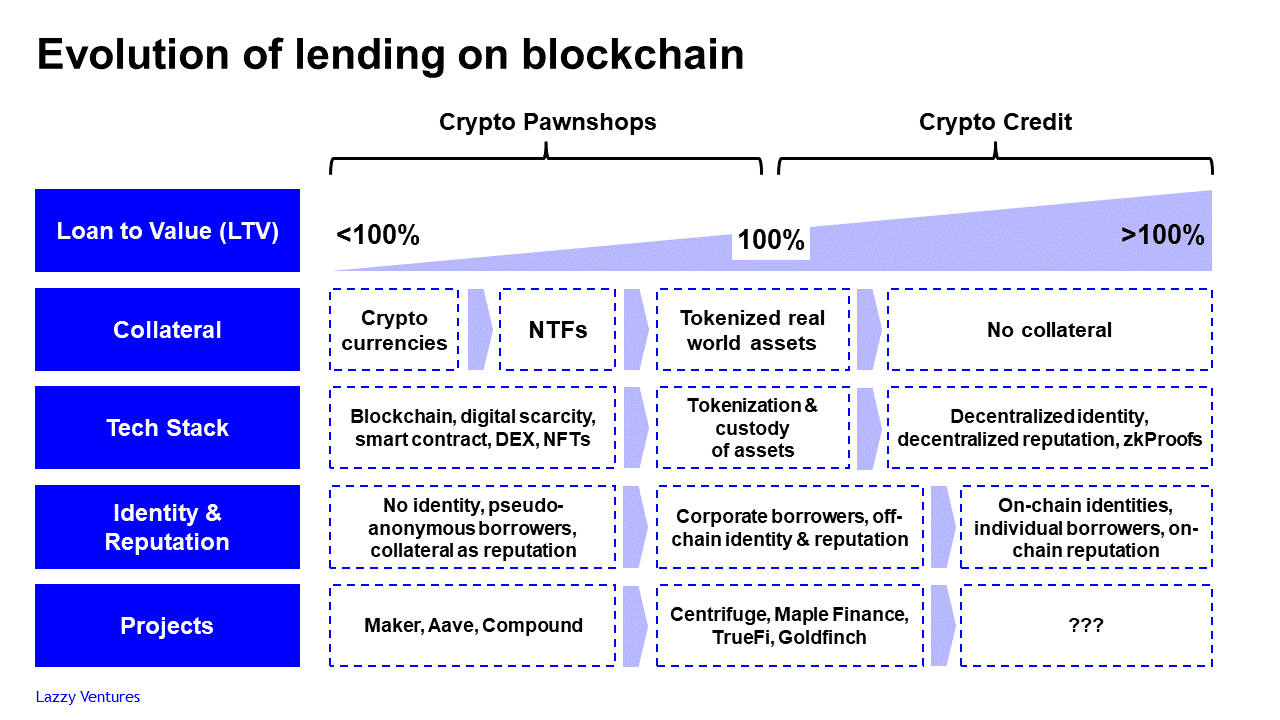

What Is Un(der) Collateralized Crypto Lending?

This evolution in blockchain financial markets allows institutional borrowers to access credit with little or no pledged assets, setting it apart from the overcollateralized loans common in the space. Instead, lenders assess risk using advanced analytics, including credit ratings, observable on-chain financial activity, and, in some cases, audited self-reported finances. While inherently riskier, unsecured loans offer:

- Flexible collateral requirement: Some models remain fully uncollateralized, while others use semi-collateralized frameworks to mitigate lender exposure. However, eliminating the need to pledge security improves market liquidity.

- Creditworthiness assessment: Borrower reputation is evaluated using blockchain-based credit histories, wallet activity, and external verification of assets and liabilities.

- Higher interest rates, smaller loan sizes: Lenders compensate for elevated risk with adjusted pricing structures.

Opportunities and Innovations

Increased Capital Efficiency

Unsecured lending frees liquidity by removing the capital lock-up burden, boosting value circulation. This flexibility can:

- Expand the digital economy by supporting borrowing without restricting asset mobility, keeping crypto balances functional while unlocking additional liquidity. A Nigerian merchant using stablecoins could prove its creditworthiness on-chain and secure a USDC loan from a London investor to restock inventory—without locking up working capital.

- Enhance efficiency by letting borrowers leverage creditworthiness—not just collateral—reducing friction in markets. A Web3 gaming studio might secure funds for development based on its NFT sales history and proof of digital asset balances.

- Improve market liquidity, by increasing capital availability, tightening spreads, and enhancing the depth of order books across trading and lending markets. Picture a market maker borrowing $10M based on balance sheet strength to provide tighter bids on an exchange, fueling smoother trades without tying up $15M in collateral.

Creative Credit Assessments

Innovations in blockchain-based credit scoring are transforming borrower evaluation in unsecured lending:

- Privacy-preserving risk assessments: Zero-knowledge proofs (ZKPs) and other cryptographic methods enable lenders to verify borrower health without requiring full data disclosure, striking a balance between risk transparency and user privacy.

- Credit ratings based on public data: Statistical tools can generate credit scores based on publicly available on and off chain information.

- Holistic reputation analysis: Borrowers can enhance their credibility by linking their on-chain activity with off-chain data sources, including verified social media accounts, executive professional profiles, and transaction records.

- Dynamic risk pricing: Machine learning models analyze historical repayment behavior, wallet interactions, and credit history across multiple DeFi protocols, allowing for tailored rates and terms that fit the borrower’s risk.

- Progressive credit-building models: Borrowers with limited histories can gradually access higher credit limits by successfully repaying smaller, incremental loans, fostering trust over time.

Financial Inclusion

While unsecured lending opens new avenues for users in emerging markets and those without significant crypto holdings, access to capital must not come at the expense of creditworthiness. Advances in risk assessment and liquidity provisioning ensure that lending remains responsible and sustainable. Here’s how it works without wrecking the system:

- Targeting high-potential borrowers: Rather than indiscriminately expanding credit, unsecured lending can focus on institutional borrowers with verifiable financial behaviors and sound credit histories, using privacy-preserving analytics to maintain responsible lending standards.

- Reducing cross-border frictions: Improved liquidity and seamless transaction settlement via blockchain networks enable more efficient capital allocation, providing high-quality borrowers in underserved markets with better financing opportunities.

- Ensuring sustainable credit access: By leveraging advanced risk frameworks, reputation systems, and verifiable financial data, lenders can extend credit to previously overlooked borrowers while maintaining strong risk management cultures.

- Bridging the funding gap for businesses and entrepreneurs: Unlocking new sources of capital through unsecured lending empowers high-potential enterprises to grow and scale, particularly in regions where traditional banking infrastructure is underdeveloped.

Challenges to Scaling Unsecured Lending

The improvements above come with frictions, and moving away from overcollateralization requires caution:

- Risk of Defaults: Past attempts, like Goldfinch, faced setbacks due to weak risk models. Defaults can undermine confidence and deter lenders, with crypto volatility further complicating risk pricing and capital availability.

- High Interest Rates: Higher risk demands higher yields, attracting income-seeking lenders but perhaps limiting borrower access and slowing adoption.

- Regulatory and Market Risks: Higher rates of default may trigger stricter oversight on capital/deposit gathering, fraud, and stability. Further, crypto’s volatility adds complexity to crafting viable loan terms.

- Decentralization introduces new complexities: Removing central coordination points creates governance challenges, heightens risk exposure, and slows responses in dynamic markets.

Projects Driving Innovation

Accountable

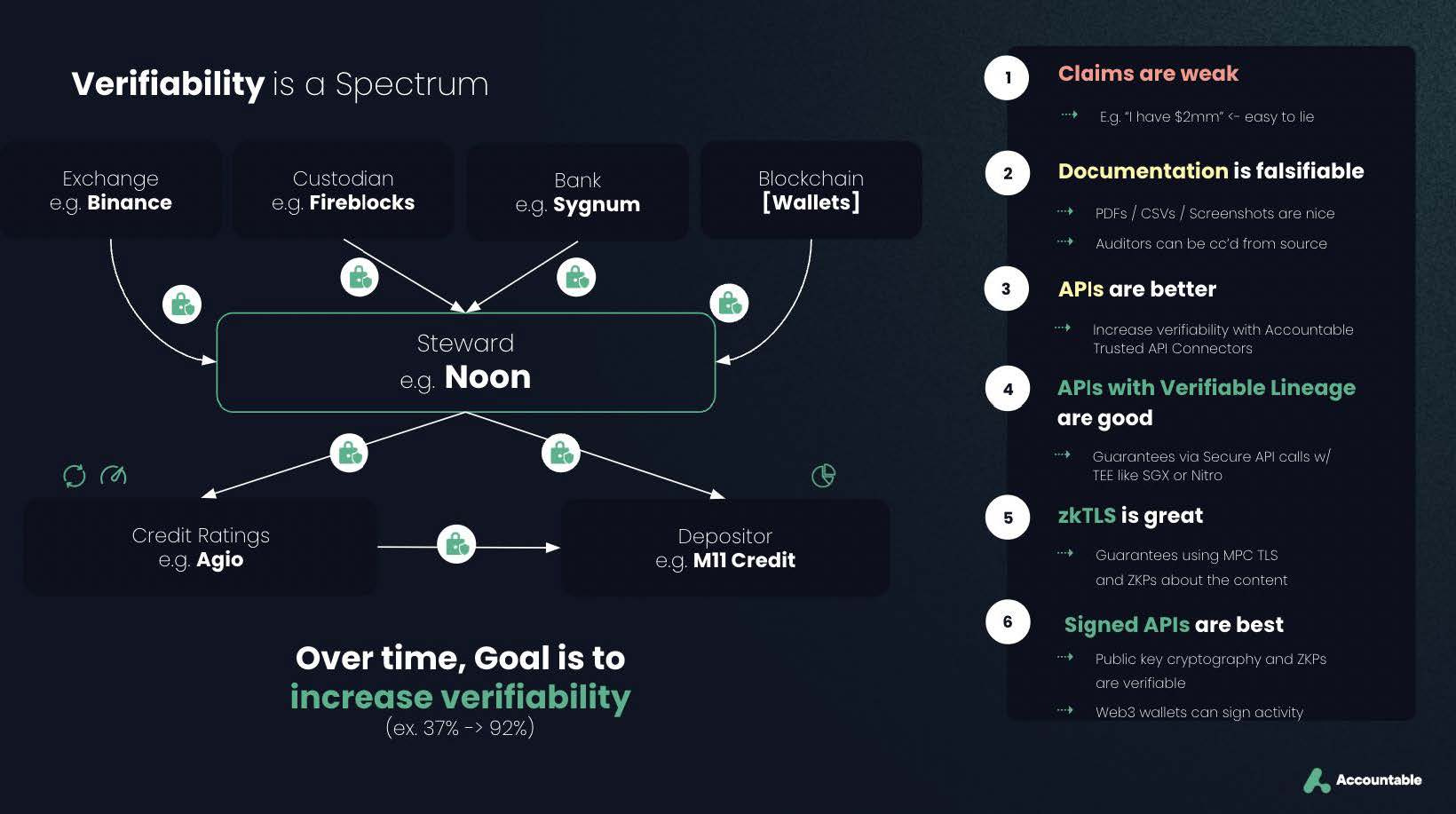

Accountable is redefining risk management in unsecured lending by enabling real-time verification of off-chain and on-chain financial activity—without exposing sensitive data. Borrowers can prove their activity across exchanges, brokerage accounts, banks, and DeFi platforms without revealing API keys or wallet addresses. This privacy-first approach is critical, as trading firms and market participants must protect their proprietary strategies from data leaks.

Using advanced cryptography, Accountable ensures institutional lenders, borrowers, and DeFi platforms can scale unsecured lending with controlled risk exposure. To further enhance transparency and lender confidence, Accountable is launching fully customizable vaults. These vaults allow borrowers and credit funds to structure their credit facilities while integrating real-time verifiability, fostering trust and liquidity in the space.

Accountable’s Tech Stack

Agio Ratings

Agio Ratings is a credit and risk analysis firm focused on the digital asset market. With a team of seasoned financial professionals, statisticians, and data scientists, it has developed proprietary risk models that capture the market’s unique and volatile risk factors. The organization is trusted by leading risk teams in the industry and backed by globally renowned investors, including Superscrypt, Portage, and MS&AD Ventures.

Institutional Credit Underwriters

- Cicada Partners: Facilitating credit access using alternative scoring methods and crypto funding rails, Cicada Partners focuses on driving stablecoin adoption by structuring innovative lending programs for underserved borrowers. Their approach leverages digital asset tools with traditional underwriting frameworks and off-chain legal structuring, ensuring more users can access crypto credit without excessive collateral requirements.

- M11 Credit: Developing institutional-grade credit solutions tailored for professional investors, M11 Credit works closely with DeFi protocols and traditional lenders to bridge the gap between crypto-native and traditional credit markets. By implementing stringent risk controls, portfolio diversification strategies, and strategic partnerships, M11 Credit is paving the way for broader institutional adoption of lending in crypto.

- Tesseract: Tesseract is a leading provider of crypto yield solutions, enabling platforms like exchanges, wallets, and custodians to offer secure and compliant yield products. By integrating seamlessly through APIs and web apps, Tesseract helps partners unlock new revenue streams while maintaining full regulatory compliance. Their product suite includes Market Maker Lending, BTC Staking, and Managed DeFi, designed to deliver risk-adjusted returns with transparent risk management.

Why Unsecured Crypto Lending Matters

Traditional unsecured credit (cards, personal loans, and revolving corporate lines) powers economic activity worldwide. Crypto-native unsecured lending introduces new efficiencies and challenges:

- Greater transparency and reduced friction: The open and verifiable nature of public blockchains streamlines data access, allowing lenders to make more informed decisions with real-time borrower insights. This reduces reliance on intermediaries and enhances credit availability for qualified borrowers.

- Improved risk assessment through hybrid data sources: By integrating off-chain financial data with on-chain reputation scores, lending models can combine the best of traditional finance and DeFi, leading to more reliable borrower evaluations and responsible credit issuance.

- Privacy concerns and data exposure: As financial transactions become increasingly intertwined with public blockchains, borrowers and lenders must navigate the trade-offs between transparency and confidentiality. Privacy-enhancing solutions will be critical in balancing risk management with user security.

- Potential for institutional integration: A hybrid approach, blending decentralized innovations with traditional credit risk methodologies, should pave the way for more institutional players to enter the unsecured crypto lending space, offering new liquidity sources and compliance-driven safeguards.

The New Standard: Sustainable Crypto Lending

The 2022 crypto crash taught a harsh lesson: fraud thrived when risk management relied on rumors, static data, and “trust me, bro.” Testing a counterparty meant pulling loans—no tech could fill the transparency gap. Now, unsecured lending’s future hinges on live, verified financials paired with credit ratings and classic underwriting. With real-time financial visibility, lenders and agencies can assess risk using verified data, reducing fraud and enabling faster, more informed decisions. It’s a step toward a capital-efficient, inclusive system—if balanced with smart risk controls. As Accountable, Agio Ratings, and other institutions refine this space, now is the time to engage—whether as a lender, borrower, or investor—helping shape the next era of digital credit markets.

Q: How does unsecured crypto lending differ from traditional crypto lending?

A: Traditional crypto lending relies on overcollateralization, meaning borrowers must pledge more assets than they borrow to reduce lender risk. In contrast, unsecured crypto lending allows borrowers to access credit without or with minimal collateral, instead relying on credit scoring, risk analytics, and borrower reputation to assess risk.

Q: What are the main risks associated with unsecured crypto lending?

A: Unsecured lending introduces default risk, as there’s no direct collateral backing the loan. Around the world, regulatory and legal developments and uncertainty remain key risks. In addition to market volatility, regulatory uncertainty, and governance challenges in decentralized finance (DeFi) make risk assessment more complex in those markets. However, innovations in on- and off-chain credit scoring, privacy-preserving risk assessments, and real-time financial verification help mitigate these risks.

Q: How are lenders assessing borrower risk without collateral?

A: Lenders use a combination of on-chain financial activity, credit ratings, decentralized reputation systems, and verified off-chain financial data. Privacy-preserving technologies, such as zero-knowledge proofs (ZKPs), allow lenders to verify financial health without exposing sensitive borrower information.

Q: Why is unsecured crypto lending important for institutional adoption?

A: Institutions require capital efficiency and credit markets similar to traditional finance. Unsecured lending enables institutional borrowers to access liquidity without tying up significant capital, enhancing market efficiency. It also bridges crypto-native lending with traditional financial risk frameworks, making it more viable for hedge funds, market makers, and enterprises. Historically, leverage has been a key driver of financial market growth—and crypto is no exception. Unlocking responsible leverage is critical for the next phase of institutional adoption.

Q: How does real-time financial verification change the game?

A: Unlike traditional risk assessment, which relies on static, self-reported data, unsecured lending platforms now leverage live, verifiable financials. Tools like Accountable allow borrowers to prove financial activity across exchanges, banks, and DeFi in real-time—without exposing private data. This enhances transparency, reduces fraud, and increases lender confidence

.png)