While headlines fixate on tariffs and trade wars, a quieter shift is forming where crypto and traditional finance meet: insurance. That’s right—perhaps one of the least buzzy sectors—may turn out to be one of the most consequential in integrating blockchain’s core capabilities into everyday financial infrastructure.

The promise here isn’t about speculative upside. It’s about underwriting downside. And in doing so, it may help close the trust gap between the old world and the new.

Why Insurance? Why Now?

Insurance and blockchain are natural allies. Both are coordination tools. Both rely on shared truths and probabilistic outcomes. And both depend on efficiently assessing and pricing risk.

From microinsurance for crop failures to coverage for DeFi exploits, the sector is quietly experimenting with blockchain as a trust layer. And while progress has been slow, the stakes—and opportunities—are growing.

According to BCG, blockchain-related revenues in insurance could reach $37 billion by 2030, growing at a 70% annual clip. Over 60% of insurers are already investing in blockchain, and 80% of insurance execs believe the tech can unlock meaningful efficiencies.

Where Innovation Meets Risk Management

At their core, both blockchain and insurance are about distributing risk through trust. The alignment is elegant:

- Trust: Immutable records provide a single source of truth

- Transparency: All authorized participants access the same data simultaneously

- Immutability: Data can’t be changed without consensus, deterring fraud

These traits directly address longstanding industry issues—fragmented data, high administrative costs, and limited trust between stakeholders.

Transforming Core Insurance Operations

Smart Contracts: The Automation Revolution

Smart contracts might be blockchain’s most radical contribution to insurance. These self-executing agreements can automatically verify claims by linking to real-world data sources—like patient health records or satellite-based weather indices.

Parametric insurance is an ideal use case: payouts triggered by pre-defined events (e.g., rainfall below a certain level), with no need for subjective assessments. With on-chain oracles feeding this data, the model is low-overhead, transparent, and fast.

Fraud Detection: Immutable Advantages

Insurance fraud costs the industry billions. Blockchain can curb this by linking siloed databases and creating tamper-proof audit trails. Insurers can spot red flags early and prevent fraudulent payouts—before they happen.

Interoperable Data: Breaking Down Silos

Blockchain enables interoperable, privacy-preserving data repositories. In health or life insurance, electronic health records tied to wearable data could allow real-time risk assessments and dynamic pricing—encouraging healthy behaviors via premium incentives.

Streamlined Underwriting: From Weeks to Minutes

With permissioned blockchain access to verified customer data, insurers can dramatically accelerate underwriting. According to Deloitte, real-time underwriting can boost conversion rates from 70% to nearly 90%. That’s not a marginal improvement—it’s a business model shift.

Insuring Crypto Itself: The New Frontier

Ironically, one of blockchain’s clearest insurance use cases is... crypto itself.

The digital asset market has lost billions to hacks, exploits, and lost keys. Insurance is the safety net that can make crypto palatable to institutions—and the retail crowd.

Emerging product categories include:

- Custodial Insurance – Cold wallet risk coverage

- Smart Contract Coverage – Protection for dApps and DeFi platforms

- Hot Wallet/Crime Insurance – Coverage for exchanges and DAOs

- Slashing Protection – For validators and stakers

Projects like Nexus Mutual and Etherisc are building DeFi-native insurance protocols. They remain small but meaningful steps toward risk markets native to the crypto ecosystem.

Case Studies: Lessons in What (Not) to Build

Blockchain’s insurance journey offers rich lessons. Two stories stand out.

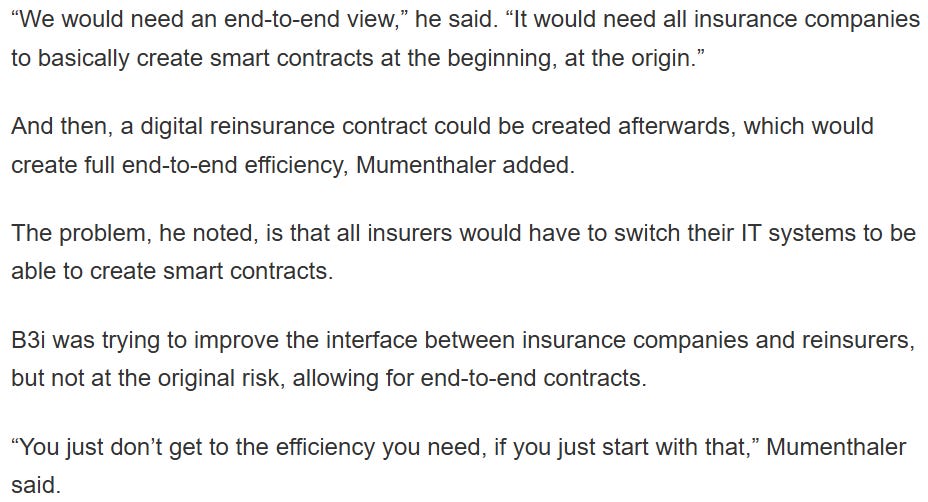

B3i: Ambition Meets Reality

The Blockchain Insurance Industry Initiative (B3i), backed by heavyweights like Allianz and Swiss Re, aimed to revolutionize reinsurance with shared ledgers. It promised streamlined claims, accounting, and data sharing. But in 2022, B3i folded, unable to secure $20 million in funding. Why? It chased too many goals at once, was bogged down by complex governance, and failed to to prove value.

The takeaway: the integration of blockchain technology with traditional finance should be explored in increments, operators shouldn’t chase tech for tech’s sake. Clear focus and pull-driven demand are non-negotiable.

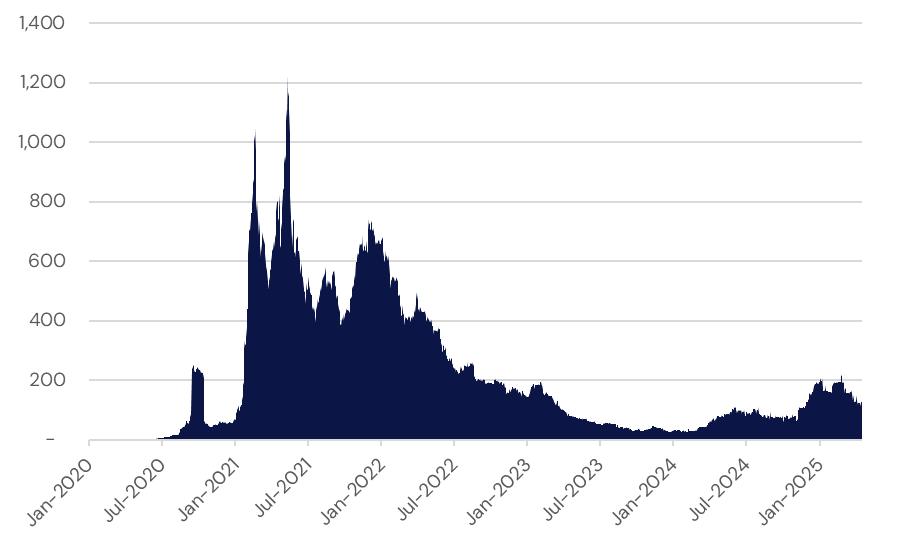

Nexus Mutual: DeFi’s Quiet Win

Nexus Mutual, a decentralized insurance DAO, shows what’s possible when focus meets execution. It has issued $5.5 billion in policies for crypto risks—smart contract failures, exchange hacks—and processed over $18M in claims while staying solvent. Its community-driven model resonates in DeFi, but growth has plateaued. Scaling beyond crypto, diversifying risk pools, and weathering bear markets remain hurdles.

Active Nexus Mutual Cover Value (in millions, USD)

Nexus proves blockchain can work in insurance—but product-market fit isn’t enough. Distribution and resilience are just as critical.

Barriers to Scale: Why Blockchain Insurance Hasn’t Broken Through

Despite its clear potential, blockchain’s integration into insurance has been anything but smooth. One of the biggest hurdles remains regulatory uncertainty. The rules around digital assets—and by extension, blockchain-enabled insurance—are still in flux. This ambiguity complicates everything from product design to distribution. As a result, companies are left building in gray zones, which stifles ambition and slows execution.

Technical and operational challenges add another layer of friction. Many blockchain networks still face limitations in processing speed, while integrating new systems with legacy IT infrastructure remains an expensive and complex task. Privacy concerns also linger. Blockchain’s transparency is a strength in many contexts, but in industries like health and life insurance—where data protection is paramount—it can quickly become a liability. Advancements in technology like zero-knowledge proofs, and fully-homomorphic encryption are encouraging, but without clear pathways to balancing transparency and compliance, meaningful adoption will remain slow.

The insurance industry’s conservatism is another major factor. With so many stakeholders—insurers, reinsurers, brokers, regulators, and customers—achieving consensus is inherently difficult. Add to that the reality that blockchain’s short-term ROI is hard to quantify, and you end up with a sector reluctant to take on big transformation bets. Moreover, competitive dynamics discourage the kind of data-sharing blockchain thrives on. For insurers used to guarding proprietary information, the notion of feeding a shared ledger—even in a permissioned context—can feel like a bridge too far.

Together, these barriers help explain why most blockchain insurance efforts remain stuck in pilot mode. The technology is viable. The demand is there. But the path to scale is slow and full of friction—a theme likely to persist for the near future.

Strategic Playbook: How to Get It Right

Blockchain’s potential in insurance is undeniable, but success demands strategy. Here’s how to move the needle:

- Target High-Impact Use Cases: Focus on sweet spots like parametric insurance (e.g., weather-triggered payouts), microinsurance for underserved markets, or reinsurance data flows. These deliver clear wins without overhauling entire systems.

- Collaborate Smartly: B3i’s failure doesn’t discredit partnerships—it highlights the need for lean governance. Streamlined consortia, industry standards, and regulatory dialogue can align stakeholders. Firms like Aquanow, specialists in digital asset integration, help bridge traditional financial infrastructure with crypto’s agility.

- Invest with Discipline: Balance pilots with capability-building. Diversify bets—some incremental, some disruptive—and reassess regularly. Internal expertise, via training or partnerships, is as vital as tech.

Closing Thoughts: Insurance as a Trojan Horse

Here’s the big unlock: insurance could be crypto’s backdoor to the mainstream. Not by minting millionaires, but by making risk palatable. When stablecoin treasuries carry A-rated coverage, staking losses are insured, and cold wallets are secure, institutions won’t just test the waters—they’ll dive in. Blockchain-powered insurance could also narrow the global protection gap, bringing microinsurance to billions in underserved regions, formalizing trust where informal systems once ruled.

The road isn’t smooth. B3i’s collapse shows the peril of overreach, and even successes like Nexus Mutual face scaling pains. Yet the fundamentals—trust, transparency, efficiency—are too compelling to ignore. Insurance may lack crypto’s sizzle, but its role in anchoring digital finance is foundational. As blockchain matures and regulations clarify, this convergence could redefine how we manage risk in a digital age.

.png)